| Having trouble viewing this email? Click here |

|  |

| Action Insight | Candlesticks Trades | Markets Summary | Action Bias | Top Movers | Daily Technicals |

| Calendar | Elliott Wave Trades | Markets Volatility | Pivot Points | Heat Map | Daily Fundamentals |

| Action Insight Market Overview | Markets Snapshot |

Daily Report: Yen Rallies as Intervention Prospect Waned on Kan's WinYen strengthens to new 15 year high against dollar today after Naoto Kan defeated Ichiro Ozawa in the party leadership election by a margin of 721-491 and remained Prime Minister. Ozawa advocated intervention to weaken the yen and was believed to be more aggressive on it. Kan's win suggests that Japan's stance on intervention would likely be status quo and traders quickly sell USD/JPY through recent low of 83.33 to as low as 83.10. Elsewhere, New Zealand dollar remains generally after poor retail sales data while Sterling is pressured by the bad housing data. |

|

| Featured Technical Report | |

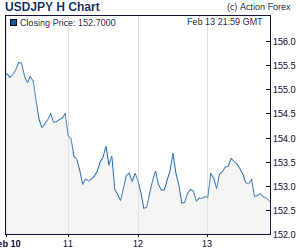

USD/JPY Daily OutlookDaily Pivots: (S1) 83.35; (P) 83.86; (R1) 84.21; More. USD/JPY's down trend resumes by taking out 83.33 and reaches as low as 81.30 so far. Current fall is expected to continue towards 80 psychological level. Nevertheless, downside momentum is not too strong yet as 4 hours MACD is bounded inside converging range. So the downward spiral path could be bumpy. But in any case, outlook will remain bearish as long as 84.37 resistance holds. Break of 84.37 is needed to be the first sign of shot term bottoming and will turn focus to 85.89 resistance for confirmation in such case. |

| Forex Brokers | ||||||

|

| Special Reports |

Preview of SNB Meeting: No Immediate Need for Rate HikeThe SNB will maintain the 3-month LIBOR target at 0.25% for an 18th month in September. Although economic growth has exceeded the central bank's expectations, inflation remained moderate. There's no immediate need for a rate hike at the moment. Concerning appreciation of Swiss franc, the SNB will reiterate its stance but we doubt much will be done in curbing the rise. Preview of RBNZ Meeting: A Pause in SeptemberAfter raising the policy rate at 2 consecutive meetings, we expect the RBNZ to leave the OCR unchanged at 3% this month. Both of growth and inflation have not evolved as strong as the central bank forecast in June and the earthquake in Christchurch last week may lead policymakers to revise down the economic forecasts. Given heightened uncertainty in the domestic and foreign growth prospects, the RBNZ will take a more cautious stance in determining the next step in its monetary policy. Growth Remains Robust in China, Increases Likelihood of Soft-LandingThe latest set of macroeconomic data from China indicates domestic demand in the world's second largest economy, as well as the biggest growth driver, remained resilient in August. This soothed market concerns that the government's cooling measures implemented earlier in the year would cause an abrupt brake on economic expansion. Developments in August generally beat expectations with industrial production and fixed-asset investments showing strong rebounds while retail sales remaining robust. Inflation stayed above official target of +3% but should being to ease in coming months. We expect the government will reiterate its tight policy stance for the rest of the year but is unlikely to accelerate the tightening schedule. |

| Economic Indicators Update |

Attend The Futures & Forex Expo Las Vegas, September 23-25, at Caesars Palace, where industry experts will help Forex & Futures traders make profitable trading decisions. Register FREE | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Candlesticks and Ichimoku Intraday Trade Ideas | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Trade Idea: USD/CHF – Sell at 1.0115Dollar's selloff from 1.0278 was much stronger than expected and once the indicated support at 1.0136 as well as the Ichimoku cloud area was penetrated, decline accelerated and recent downtrend resumed this morning to as low as 1.0008 before recovering. Outlook remains bearish for test of psychological support at 1.0000, below would extend weakness to 0.9993 (50% projection of 1.0630 to 1.0060 measuring from 1.0278) but reckon downside would be limited to 0.9926 (61.8% projection) and reckon 2009 low of 0.9910 would hold due to oversold condition. Trade Idea: EUR/USD – Sell at 1.2920Although yesterday's rally suggests near term rise from 1.2642 may extend gain towards resistance at 1.2920, as broad outlook remains consolidative, upside would be limited and overbought condition should cap price below 1.2954 (50% projection of 1.2675 to 1.2893 measuring from 1.2845) and bring retreat later. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Suggested Readings | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Fundamental Highlights

Technical Highlights

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||

No comments:

Post a Comment